Learn how RBI compliant eMandate infrastructure helps Indian lenders secure recurring payments with encryption, authentication, audit trails, and compliance.

Ask any collections head at an Indian NBFC what keeps them up at night, and the answer rarely changes. It is not delinquency rates.

It is the fragility of the recurring payment stack that sits underneath every EMI, every subscription drawdown, every loan repayment cycle. And at the centre of that stack sits your emandate infrastructure.

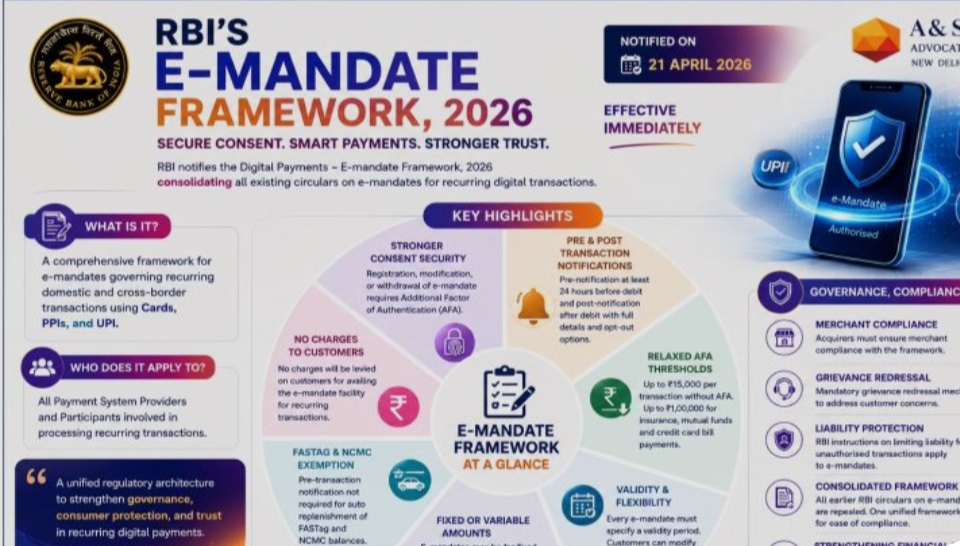

The Reserve Bank of India has spent the last four years tightening the screws on how digital debits work.

From the 2021 recurring payment guidelines to the more recent additional factor authentication rules, the compliance surface has widened considerably.

If your lending operation still treats emandate setup as a plug-and-play integration, you are exposed in ways that will surface only when an audit lands on your desk.

Here is the thing. RBI compliance is no longer a checkbox. It is an architectural decision.

Why the RBI framework demands more than surface-level compliance

The regulatory logic behind emandate is straightforward. Borrowers need protection from unauthorised debits.

Lenders need certainty that the debit will actually go through. Banks need a settlement rail that can be audited end to end. Getting all three to coexist is where most lenders stumble.

A compliant flow has to handle consent capture, authentication, pre-debit notification, the actual debit, exception handling, and revocation.

Each of those has its own RBI stipulation. Skip one, and you are looking at customer complaints at the banking ombudsman, followed by internal notices you would rather not receive.

The security features every lender should audit right now

Before you evaluate any vendor or in-house build, run your current setup against these non-negotiables.

- End-to-end encryption on all customer authentication data, both in transit and at rest

- Two-factor authentication during mandate registration, aligned with NPCI’s AFA framework

- Pre-debit notification sent to the borrower at least 24 hours before the debit attempt

- Immutable audit logs for every consent, modification, and revocation event

- Tokenisation of bank account details so raw account numbers never sit in your primary database

- Real-time reconciliation with the sponsor bank

Miss any one of these, and you have a compliance gap. The uncomfortable truth is that many mid-sized NBFCs are running on infrastructure that satisfies three or four of these, not all six.

Consent, authentication, and the audit trail question

This is where things get interesting.

RBI’s position on borrower consent has evolved from a signed form to a fully digital, cryptographically verifiable event.

Your emandate infrastructure must capture consent in a format that survives a regulatory challenge two years later. Screen recordings, time stamped OTP validations, IP logs, device fingerprints. All of it matters.

Consider a scenario. A borrower disputes an EMI debit six months after the fact. Can your system produce, within minutes, the exact consent artefact including the authentication method used, the timestamp, and the debit schedule they agreed to?

If the answer involves an engineer pulling database logs manually, you have a problem.

Fintechs building on modern rails have already solved this. Legacy lenders often have not.

For teams still working through the operational side of consent capture and mandate lifecycle, the complete emandate registration process breaks down each stage in detail and is worth reviewing before your next compliance sync.

Where most lenders quietly fall short

Talk to anyone running lending operations in India, and a few patterns show up repeatedly.

Bounce management is the first. When an emandate debit fails, the retry logic often runs blind. No coordination with the sponsor bank, no borrower notification, no updated schedule visibility. RBI expects a defined process. Most lenders have a script.

The second is revocation handling. Borrowers have the right to cancel a mandate at any time.

If your system takes 48 hours to reflect that cancellation and a debit hits in the meantime, you are the one holding the compliance bag.

Third, data residency. All emandate data must remain within India. Cloud configurations set up in a hurry sometimes route traffic through overseas regions without anyone noticing until an audit flags it.

Conclusion

The lenders who get this right treat emandate infrastructure as a first-class product concern, not a payments afterthought.

They invest in real-time monitoring, run quarterly compliance drills, and document every architectural change against the relevant RBI circular.

You do not need a hundred-person compliance team to do this. You need clarity on what the framework demands, honesty about where your current setup falls short, and a roadmap to close the gaps before the regulator does it for you.

Compliance is not a cost centre. It is the reason your lending business gets to keep operating at scale.

Strengthen your lending operations with a secure RBI-compliant eMandate infrastructure. Evaluate your payment security framework and stay audit-ready today.